fjrigjwwe9r3SDArtiMast:ArtiCont

With rising life expectancy in India, post-retirement life span is now longer than what it was earlier. According to the latest World Bank data, life expectancy in India has risen from 53-54 years in 1980 to 67-70 years in 2015. Living longer has a direct impact on your financial preparedness for retirement. While many will have an accumulated pension to fall back on, the truth is an annual price rise or inflation of 5-6% combined with the prospect of potentially living for another 20-25 years post retirement can become an expensive outcome.

A basic need for retirees is regular income. You need to take that accumulated pension amount, other savings you have piled up over the years and assets you have created and make them into a viable stream of regular income.

Large expenses like medical contingencies need to be accounted for before you estimate your regular income need, else these expenses can eat into your retirement savings. “We find that many who retire haven’t planned any medical insurance. With health costs rising, this is a risk that needs to be covered. If both spouses are not fit enough for mediclaim application to be accepted, the one who can should cover medical expenses through a policy. In its absence, a larger pool of funds will have to be kept aside for medical emergencies,” said Vivek Rege, founder and chief executive, VR Wealth Advisors Pvt. Ltd.

Financial savings and assets

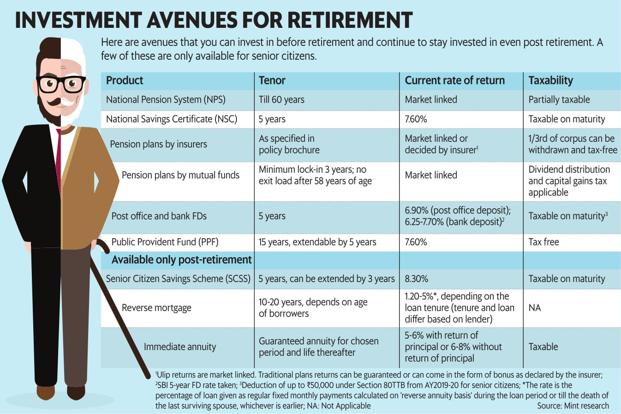

Among traditional investment choices for senior citizens are bank fixed deposits, Senior Citizen Savings Scheme (SCSS) and National Savings Certificate (NSC). Bank FDs give senior citizens an advantage by giving an interest rate that is 25-50 basis points higher than what other individuals get. The 8.3% interest on SCSS is also attractive. One basis point is one-hundredth of a percentage point.

After allocating to traditional investments and pension plans which cater to capital preservation, consider mutual fund investments as well—they are liquid, they help you get regular payouts and let you access the lump sum in case of any emergency. For debt funds, your holding period can be between 6 months and 3 years, equity and balanced funds will require you to remain invested for at least 5 years.

Yogita Dand, Mumbai-based certified financial planner and co-founder, AskY Financial Services, said, “Invest in SCSS and Pradhan Mantri Vaya Vandana Yojana, in which you can invest up to ₹ 15 lakh. With the rest, create systematic withdrawal plans (SWPs) from investments in large-cap equity or balanced funds.” An SWP from an equity-oriented fund works if you have invested in equity before and have accumulated profits. Given the need for capital preservation post retirement, if one does not have any equity exposure, then SWP should be done from short-term income funds or other fixed income funds that give stable returns.

Physical assets

Traditionally, most Indian families invest in a house. In many cases, people own a house but have inadequate cash flow to meet their expenses or lifestyle, but still do not want to move to a new smaller house or on rent. For such persons, there is reverse mortgage.

To opt for reverse mortgage, you must be the home owner and above 60 years of age. It’s like mortgaging your house to the bank, and getting a loan which comes to you as regular payouts. The eligibility depends on age, value of the property, interest rates and tenure of payout. The tenure can be for up to 20 years; the longer the tenure, the lower will be the payout.

Punjab National Bank, for example, pays ₹ 435 per lakh per month and ₹ 101 per lakh per month for a tenure of 10 and 20 years, respectively. For a ₹ 80 lakh loan, this will come to a monthly payout of ₹ 34,800 for 10 years and ₹ 8,080 for 20 years. The current rate is about 11.35% per annum, and is revised every five years.

Even if the tenure gets exhausted, you can continue living in the house. On death, legal heirs can keep the house by repaying the loan with interest. Else, bank can sell the house to recover the dues and pay the remaining to the legal heirs.

It’s been a decade since reverse mortgage was introduced in India, but there are few takers for it. “There is lack of awareness, neither the government nor the lenders ever tried to make it popular. Low payout, lack of understanding and complex process of borrowing are other deterrents,” said Manoj Pandey, director, Mainstream Investments Advisors Pvt. Ltd, a Delhi-based financial planning and wealth management firm.

What you should do

Remember that structuring a SWP, choosing appropriate funds or even deciding to go for a reverse mortgage is not simple.

Your mix of fixed-return products like FDs, small savings schemes and annuities and market-linked products like debt and equity mutual funds will depend on your existing savings pile and your need for capital preservation.

Also, fixed return products work best if you are in the 10% or 20% income tax bracket. For those paying 30% plus income tax, a mix of mutual funds is more efficient. Don’t lock all your money in locked-in products like deposits, bonds and annuities.