fjrigjwwe9r3SDArtiMast:ArtiCont

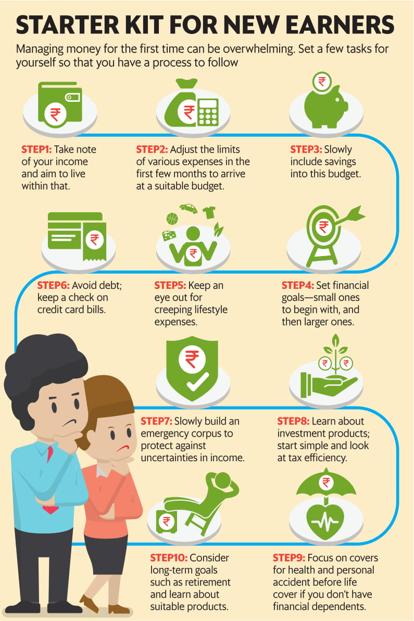

Managing money can be a daunting task when you are young, say, in your 20s. You have to wrap your head around earning your first income and deal with things like paying rent, utilities and other expenses on your own for the first time. Your first paycheck is the trigger for you to start being money responsible and develop good money habits, if you have not already done so. Here are some elements of financial planning that can help bring some discipline into the way you deal with your money.

Budget for clarity and control

A budget takes the guesswork out of your finances. List your income and expenses. A budget helps you limit the expenses to the available income. Once you have developed this discipline, the next step is to include savings into your budget. To build a budget, it is important to first track, list and categorise your expenses. This will help you eliminate, cut-back and rationalise expenses so that you can find savings.

Don’t look for shortcuts by adopting ready-made templates or thumb rules that can at best be a stop-gap option. To get to your goals efficiently, you need to create your own budget. It should also not be so restrictive that it becomes difficult to live by it. A budget very rarely fits right the first time. Tweak and fine tune it until you find a good fit. Use technology to help you track and record expenses so that you can make and execute the budget effectively.

Keep it flexible

There are likely to be a lot of changes in the early years of earning. Your income and savings may see significant variation with shifts in jobs and places. Your goals may change frequently too. Your plan needs to be flexible to deal with these changes. Be prepared for that and re-evaluate the feasibility of the goals frequently to ensure that they continue to be realistic given your changed circumstances. Tying your savings into long-term products may not work if the goals change and you need your funds immediately. Similarly, committing to a long-term payment cycle, like a mortgage repayment, may not be suitable at a stage when your income has not yet stabilised. Just as your goals are likely to be flexible, your investment plan also needs to be flexible. This, of course, does not apply to your retirement savings that should not be assigned for any other goal. But the other investments should be capable of being reassigned should the goals change. Flexibility in investments should include the facility to redeem or exit easily unlike a product with a lock-in period or for a fixed term. It should allow you to add to your holding when your income goes up, or to continue with the investment if your goals have changed.

Focus on net worth

Understand the impact on your net worth when you make any money decisions. For example, the choice to invest in yourself by taking an education loan can lead to higher incomes, savings and investment in the future. On the other hand, control your expenses so that the higher income is not wasted away in expenses that don’t add to your wealth. Keep an eye out for creeping lifestyle expenses that can drain income and cost you financial security. Take debt with caution, especially consumption debt that will pull your net worth down.

Build an emergency fund

In the early years of your career, your income may see ups and downs as you explore your options. An emergency fund will give you protection against these uncertainties. Stock the emergency fund before you assign savings to any other goal. Be disciplined about when you will use the funds and about replenishing it when you use it. Review your emergency fund needs periodically so that it reflects your current income needs. In the absence of this cushion, you are likely to fall into debt and cause harm to your finances.

Create credit history

Try to build your credit profile right from the beginning so that you can take advantage of a good score when you want to borrow funds. Pay your bills on time and restrain from taking too much debt relative to your income. Meet your debt obligations on time and in full. Staying away from debt completely is not necessarily a good option since you then don’t have the opportunity to demonstrate disciplined repayment behaviour. Use the credit card and pay off the dues in a timely manner.

Product choices

Choose products that reflect your financial situation. For example, investing in long-term products like equity without providing yourself a comfortable emergency fund may push you into debt or force you to sell at loss if you are suddenly in need of funds. Signing up for a facility to invest the balance above a specified limit in a bank account maybe a better strategy to adopt while your savings stabilise rather than committing to a fixed, periodic investment.

Unless you have financial dependents or debt that may become the responsibility of your family in the event of your death, life insurance can be postponed for some time. There are other products that may be more important at this stage such as personal accident and disability insurance or health insurance, especially if you are self-employed. Similarly, select tax-saving products that reflect your risk preferences and investment horizon.

Your money actions cast a long shadow. Set a financial plan in place that will help you develop good money habits that will stay a lifetime and help you reach financial security.